Batteries are a key enabler of the renewable energy transition, but their deployment has been relatively slow in Europe until now. Surging pipelines across European markets will soon transform the revenue streams, and thus the business case, of batteries. By Micky Vriens, Green Giraffe Advisory.

To say batteries are taking off is somewhat of an understatement when seen globally. More than US$5bn was invested in the sector in 2022 – triple the amount a year earlier – and the market is projected to more than double to between US$120bn and US$150bn by 2030, McKinsey forecasts. Europe, however, has mostly been late to this party. Though it has been a leader in the deployment of renewables, it has been somewhat slower to build out battery energy storage systems (BESSs). But now there is significant momentum behind the market, and it is set to scale rapidly in the coming years.

Before delving into BESS markets, business models, and revenue streams, it is important to take a step back and appreciate why batteries are an essential part of the energy transition. Fundamentally, as the grid shifts to cleaner sources of power, such as solar and wind, while retiring old thermal power plants, frequency fluctuations in the grid become more pronounced. This is because thermal power plants provided inertia to the system, which solar and wind do not, which helps keep the grid within a certain frequency range.

Grid operators need to keep grid frequency within this range to maintain system stability. This is where BESS assets come into play. They can ramp up very quickly to respond to grid imbalances, thus helping grids integrate more and more solar and wind while keeping the grid stable. As such, BESS assets are a vital enabler of the energy transition.

The UK market

The UK has been Europe’s most attractive BESS market for years due to a combination of high variable renewable energy penetration (VRE) and the relative isolation of the UK grid. Solar and wind supplied 30% of electricity to the British grid in 2022 and its interconnectors have a capacity of 6GW, thus limiting the interaction with grids on the European continent. This has created a natural market for BESSs in the UK.

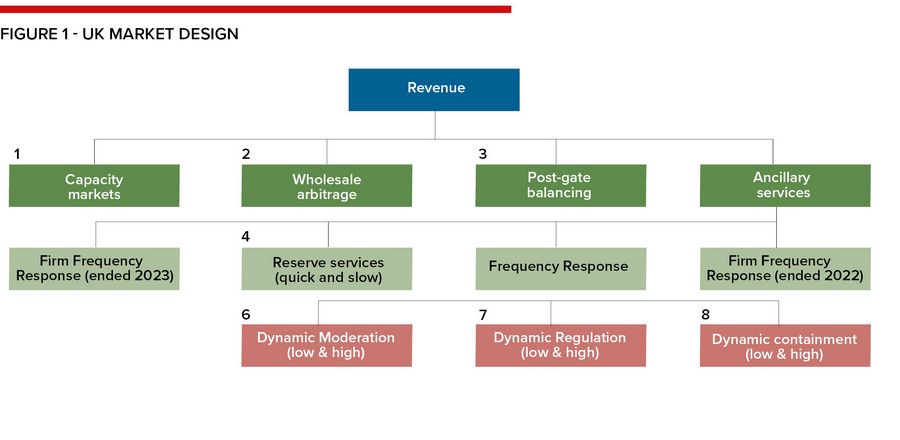

Moreover, the UK has by far the most sophisticated market design for balancing the grid, see Figure 1. By combining and optimising their participation in capacity markets, wholesale markets, balancing markets, and ancillary services, BESS operators have been able to stack revenues and generate healthy returns. Ancillary services – markets, which generally only open for seconds at a time to resolve any minor grid imbalances – have been particularly lucrative.

A clear market need and structure have facilitated the expansion of BESS capacity in the UK. By the end of 2023, the UK is expected to have installed just under 4GW, according to Modo Energy. This is more than any other European country save Germany. However, about 83% of Germany’s BESS power capacity comes from residential installations, making the UK the clear leader for large-scale BESS projects.

Nevertheless, developments across European markets are now generating significant interest among investors.

The rest of Europe

Two European countries, in particular, have grabbed headlines with developments in their BESS markets: Germany and Italy. This also reflects what Green Giraffe Advisory has heard from investors when working on BESS transactions.

Both countries have ambitious renewable energy deployment targets: Germany aims to have renewables account for 80% of power consumption by 2030, while Italy targets 65% by the same year. By some estimates, Germany will need an additional 84GWh of storage capacity by 2030 to accommodate this renewable energy build-out. Meanwhile, Italian Transmission System Operator (TSO) Terna predicts it will need 94GWh. Based on the duration, this approximately means that Germany would need anywhere between 21GW and 42GW of additional installed capacity, while Italy would require 24GW–47GW.

Thankfully, market predictions point to an ambitious build-out. By 2030, Germany and Italy are projected to install about 21GW and 9GW of BESSs, according to LCP Delta. Yet even this will not be sufficient to meet the demands of the grid – demand for these assets is only likely to increase in the future.

Recently, there has been a slew of large-scale project announcements in Germany as the market shifts away slightly from residential installations. Kyon Energy announced that it had received approval for a 137.5MW/275MWh BESS in Alfeld, Lower Saxony, while Eco Stor unveiled a 300MW/600MWh project in Wittlich, Rhineland-Palatiante. Both projects will begin construction in 2024. Additionally, utility EnBW revealed that it would be co-locating all future solar PV projects with BESSs and would eventually do the same with its wind projects.

Italy only recently became appealing as a storage market. It generated a wave of interest in 2020 with a pilot Fast Reserve auction, through which it awarded 250MW of capacity to BESS assets. In 2022, its capacity market auction awarded contracts to over 1GW of BESS projects, with Enel emerging as the clear winner. Terna has reportedly described battery storage as the “indispensable new lungs of our energy system” and project developers are moving quickly to build those lungs. Enel Green Power has already started construction on its 1.3GW pipeline in Italy, while Aura Power has received final approval for a 200MW/ 800MWh BESS project. Additionally, Matrix Renewables and Eku Energy are both developing 1GW+ BESS pipelines.

Other European markets, such as Greece, Spain, and Belgium, are also increasingly attracting the attention of developers and investors. Greece held its first auction for BESS facilities in July 2023. It was a capacity market auction, which aimed to contract 400MW of BESSs and offered developers support to the tune of €115k/MW, which would depend on the performance of the asset, and an additional €200k/MW in subsidies. The auction was massively oversubscribed – 95 offers were submitted with a total capacity of 3.3GW. Greece will hold two more auctions in the near future and it has already indicated that it will halve the subsidy to €100k/MW.

In Belgium, BESS assets emerged as the big winner in Elia’s recent capacity market auction. They represented all new-build capacity and with combined derated capacity of 357MW/1,428MWh. Meanwhile, Spain recently awarded contracts to 880MW/1,800MWh of BESS projects through its PERTE tender. The average level of support was €86k/MWh. The Spanish government has set aside €150m in subsidies to develop the BESS market – it targets 20GW by 2030. All of this indicates that there are significant developments across the markets.

Market drivers and issues

As written above, the main driver of the BESS market is the physical need of the grid to have these assets. Yet, despite this need, the BESS market would not have taken off had it not been for beneficial policy and clear regulatory regimes. The UK and Germany offered generous subsidies to help the market take off. Greece is pursuing a similar path to build out its BESS capacity as well.

Furthermore, BESS assets have been exempted from grid payments for the first 10 years of operation in Belgium and for the first 20 years in Germany. This significantly reduces their operational expenditure, improving their business case. Evidentially, these governments are prioritising the expansion of BESS capacity as a way of buttressing the grid – grid expansion is expensive and BESS assets are a cheaper way of achieving a similar end.

Ironically, in some countries the grid can be a major obstacle for BESS assets. Despite being able to help manage this, grid congestion can make it difficult for developers to obtain grid access. In fact, it is because of this that the Netherlands levies a hefty grid fee on BESS projects, calculated on a capacity basis (MW) instead of on a usage basis (MWh), unlike its neighbouring countries. These costs can account for up to 80% of a project’s opex, thus significantly deteriorating its business case. Admittedly, this is more an issue of rules and regulations than anything else.

Despite any issues the market faces, BESS assets have become and will continue to be an indispensable tool to grid operators as more renewable energy comes online. As BESS operators become more experienced, they are also increasingly able to generate healthy revenues.

Existing and emerging business models

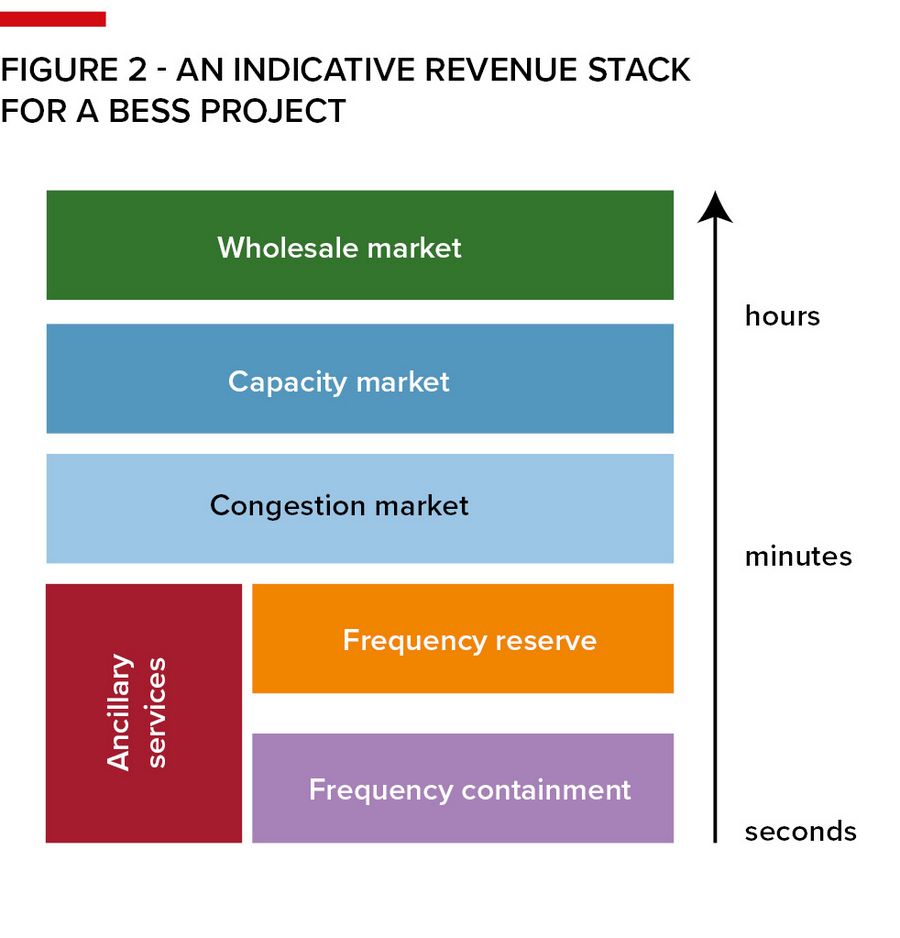

Though subsidies can kick-start a market, they cannot keep it running indefinitely. The attractiveness of BESS as investment is the ability of the asset to participate in various markets and, thus, accumulate revenue from a variety of sources. In the industry, this is known as “revenue stacking” and it can be very lucrative, see Figure 2.

Current revenue streams

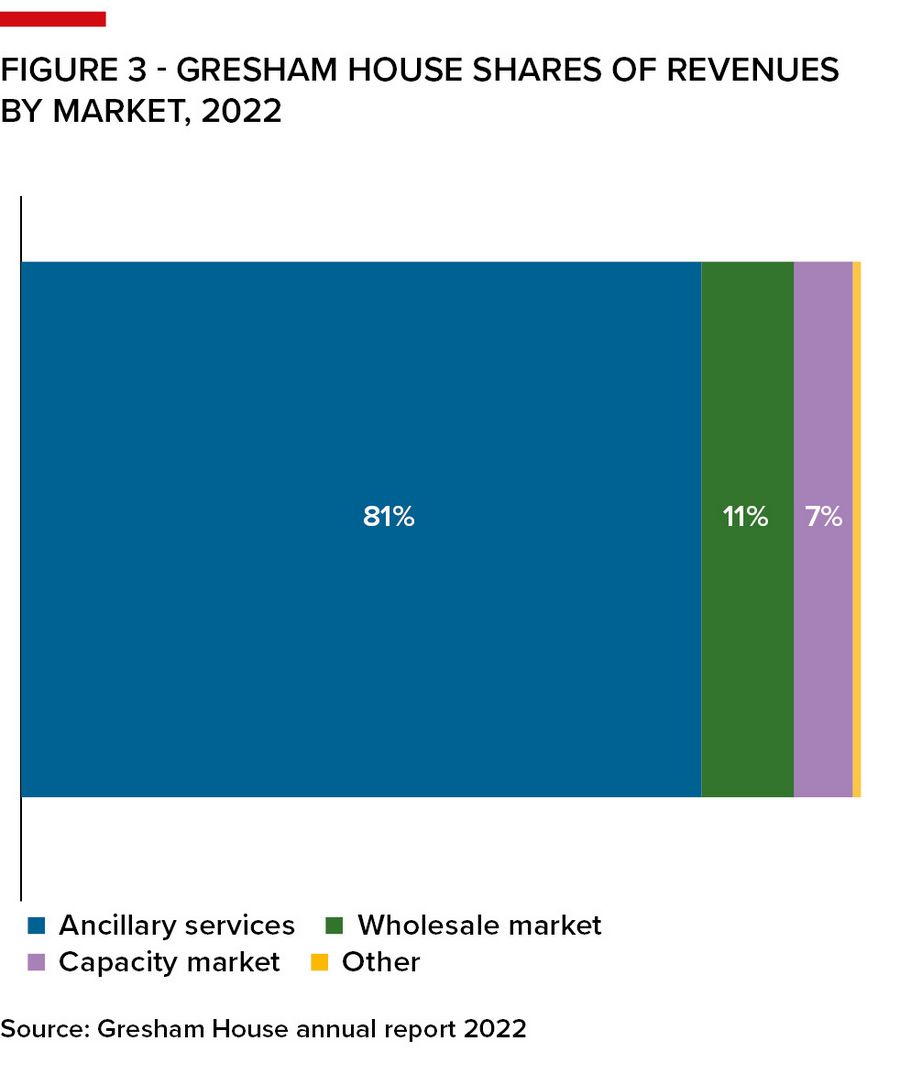

Thus far, the most important markets for BESS assets are the balancing and ancillary services markets – mainly, the frequency containment reserve (FCR) and frequency restoration reserve (FRR) markets, see Figure 3. Gresham House, one of the most experienced BESS players in the market, reportedly generated more than 80% of its revenues in 2022 through ancillary services.

Though FCR volumes are relatively small – FCR demand in Germany is only 570MW, for example – prices to resolve frequency imbalances are volatile and can generate high returns. On November 2 2023, the FCR price for a four-hour block surged to €78k for 34MW in the Netherlands. A BESS asset fortunate enough, or smart enough, to seize this opportunity would have made €2.6m in one afternoon, which would likely be half the annual revenue profile of a BESS project.

Due to its relatively small size, the FCR market will quickly become saturated and the more BESS assets there are, the lower the market volatility will be. This is already the case in Germany. As such, BESS assets need to look to other markets. The automatic frequency restoration reserve (aFRR) market is significantly larger volumetrically than the FCR and will offer BESS assets significant revenue opportunities in the years ahead. However, the technical specifications of these markets are more stringent than the FCR – an asset will need to be able to supply a maximum for a full hour – and so larger batteries currently benefit more from this market.

Given the number of markets into which BESS assets can bid – each of which with its own specifications – bidding strategies need to be highly sophisticated to optimise performance. This adds a level of operational complexity, which is unique to the BESS asset class. As such, the software that determines the bids of these projects will be vital to their performance. This is only going to become more pronounced as BESS assets need to optimise their bids across more markets.

Emerging revenue streams

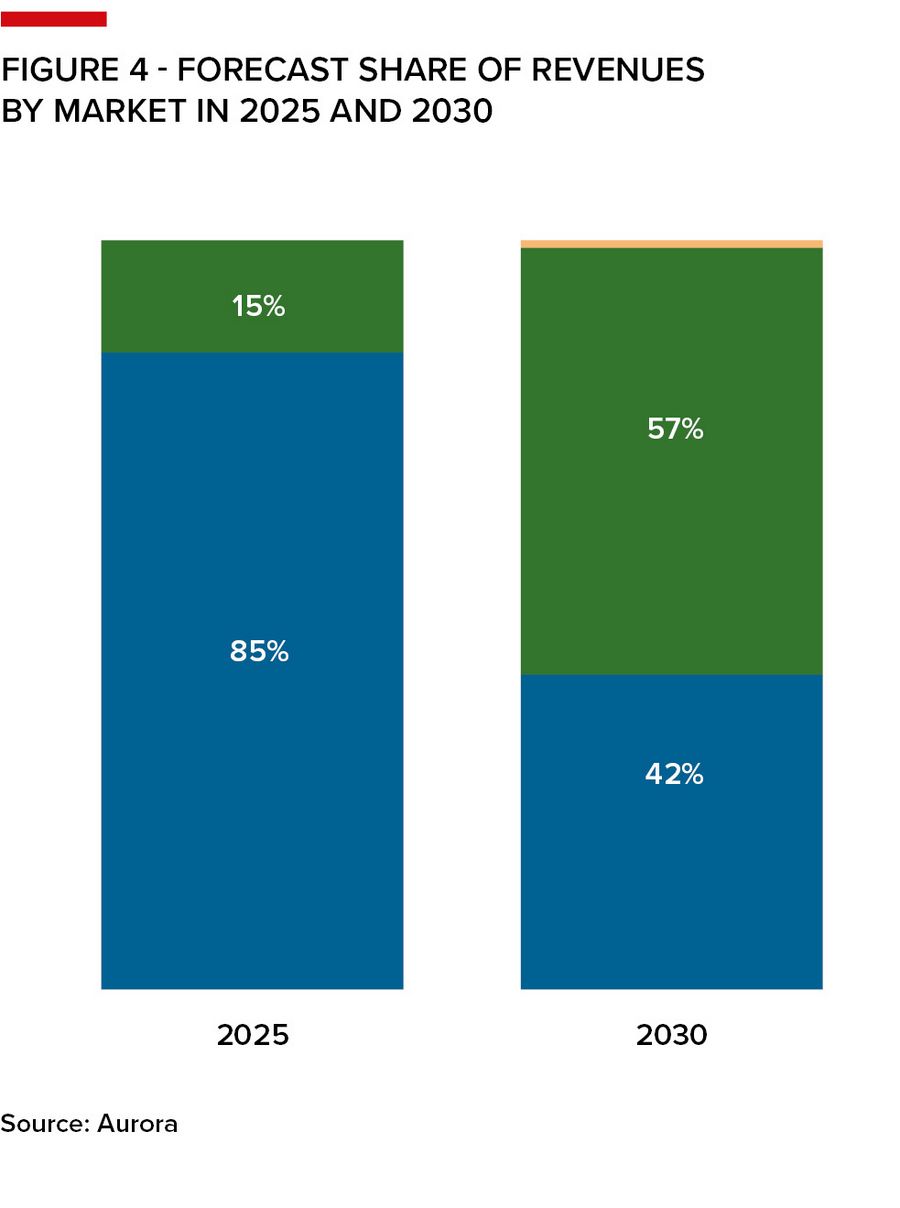

As frequency markets become more saturated, other markets, such as the wholesale and capacity markets, have become more important. That is not to say that balancing and ancillary services will become unimportant, they will just be less lucrative. By 2030, 57% of a BESS asset’s revenues will come from the day-ahead and intra-day markets instead of from balancing and ancillary services, according to Aurora modelling, see Figure 4. This is largely a result of the saturation on balancing markets and the increasing volatility in day-ahead and intraday markets as result of a higher share of variable renewable energy resources.

Additionally, capacity markets will underpin BESS projects, by generating fixed, predictable revenues over a longer timeframe. Capacity market auctions have become a policy tool to stimulate BESS deployment in various markets. Recently, in Belgium the 357MW of BESS assets that were contracted in Elia’s capacity market auction secured a tariff of €53k/MW per annum for 15-years. The increasing importance of capacity markets and wholesale markets will likely translate into projects with longer durations, which in turn, will enable them to participate in the aFRR market more thoroughly.

These tariffs provide clear visibility on long-term revenues for BESS projects – something that solar and wind developers are accustomed to, but which has eluded BESS developers so far. The lack of visibility of revenues has made it difficult for developers to raise project financing on BESS assets, thus increasing the need for equity in projects. For the most part, infrastructure funds have been all too happy to step into this market gap.

Financing BESS projects

When sculpting a debt profile for a solar or wind project, banks will differentiate between contracted revenue and merchant revenue streams – the former being more secure. As such, a bank will apply a lower debt service coverage ratio (DSCR) on contracted revenues than on merchant revenues. Any surge in electricity prices that would result in higher merchant revenues is deemed an upside, but it will not be included in the base case. Fundamentally, a lower DSCR translates into a larger loan for a project, thus reducing the equity injection needed and increasing the return of the project.

The main issue facing the BESS projects Green Giraffe Advisory has been involved with in Europe is the securing of a robust contracted offtake – providing a floor revenue – that would help raise a meaningful amount of debt. Thus, equity investors, chiefly infrastructure funds, have become key investors in this space. The situation is slightly different in the UK, where due to its track record with BESS, some banks are more than happy to size a loan on pure merchant revenues – this is a sign of a more mature market. Markets in Europe are not there yet.

Looking ahead

There is a clear need for storage and the momentum behind the market is extraordinary at this time. We at Green Giraffe Advisory do not see any reason why this will change in the coming years, but we do think the market will shift. As frequency response markets become (relatively) less important to the revenue stack, we believe that the duration of BESS assets will increase.

In fact, this can already be observed in the UK, where there is a clear shift towards batteries of a 2-hour duration, according to Modo Energy. This will vary from market to market, though. The capacity market mechanisms in Spain and Italy require durations of 4-hours – we at Green Giraffe Advisory expect to see more longer duration storage in those markets than in the UK. Though the UK will undoubtedly remain a key storage market for years to come, markets such as Germany, Italy, Greece, Belgium, and Spain will provide interesting and attractive investment opportunities for investors in the years ahead.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com