The EIB Group has partnered with LBBW in an innovative synthetic securitisation transaction to support financing of new renewable energy projects in Germany and other EU countries. By Erik Welin, loan officer, EIB, and Andre Kobinger, head of structuring and outplacement, LBBW.

The EIB Group, consisting of the European Investment Bank (EIB) and the European Investment Fund (EIF), in September 2023 issued a €175m synthetic mezzanine tranche guarantee referencing a €3.2bn portfolio of loans to small and medium-sized companies and other corporates originated by Landesbank Baden-Wuerttemberg (LBBW) in its ordinary business. By benefiting from regulatory capital relief on an existing portfolio, LBBW commits itself to new financing twice the size of the mezzanine tranche, ie €350m. The new financing is exclusively focused on new project finance lending supporting renewable energy projects such as wind farms and solar plants.

Context and rationale

The EIB is a supranational long-term financing institution owned by the 27 EU member states. It has a long track-record of supporting project finance transactions, primarily by direct participation in the projects. In order to support projects often too small for direct participation, the EIB cooperates with financial institutions by providing them with financing and/or a guarantee at preferential terms, for on-lending to eligible project finance projects.

The activities of the EIB ultimately support the public policy goals defined by its shareholders. By contributing to the financing of renewable energy projects, in these transactions the EIB contributes to the 2,030 decarbonisation targets set out in the national energy and climate plans (NECPs) for Germany and other member states, and the EU’s REPowerEU action plan.

LBBW is one of the largest banks in Germany, with a deep focus on sustainability. The bank clearly wants to support and advance the sustainable transformation of the German economy. LBBW's strong national and international track record in the growing renewable energy segment is in this context of huge help. By cooperating with the EIB Group in this third synthetic securitisation, LBBW can manage its regulatory capital on an existing loan portfolio. In exchange, LBBW uses the released capital by increasing its lending in the fast-growing segment of financing wind farms, solar plants, and other eligible renewable energy projects.

Transaction challenges

The European securitisation market has grown fast in the last couple of years. Still, compared with both the US and Asian securitisation markets it is currently significantly smaller. Securitisation transactions in the EU are therefore by themselves still kind of niche products with limited market outreach. However, having already jointly signed two previous synthetic securitisation transactions in 2021 and 2022, the EIB Group and LBBW have a successful track-record. The third transaction should therefore be reasonably straightforward, especially given that it references the same type of underlying assets in the reference portfolio. However, every transaction has its own challenges and brings something new for everyone involved.

In this transaction, the EIB wanted to focus on new climate action financing in line with its public policy goal of dedicating 50% of its financing to climate action by 2025. This required stringent EIB due diligence of LBBW’s procedures, track-record and pipeline of renewable energy project finance. In addition, the EIB requires its counterparts to be Paris Agreement aligned and meet its required environmental, social and climate criteria.

In the two earlier transactions LBBW used the freed-up capital to support small and medium sized companies with no specific/defined green angle. Therefore, the biggest challenge for LBBW with regard to this third transaction was the onboarding of the project finance team in a way that they could quickly implement all necessary processes in their daily business. This includes as well focusing on smaller PF projects and adjusting the usual internal reporting to be in line with EIB`s requirements.

Financing structure

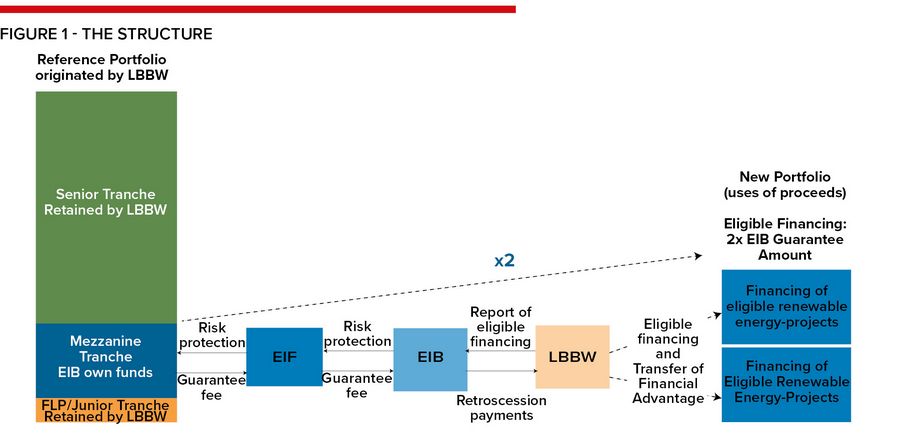

Given the dual nature of the transaction, ie both being a capital relief trade in the form of a synthetic securitisation and also an undertaking to finance new renewable energy lending, there are two parts of the financing structure. In other words, the structure can be called de-linked.

To start with, the EIB’s subsidiary, the EIF, is the EIB Group’s centre of expertise in securitisation transactions. As such, the EIF analysed the existing reference portfolio of existing loans to small and medium-sized companies and other corporates. The final portfolio was selected in compliance with a number of different criteria, eg concentration limits, obligor limits, granularity thresholds, maturity, LBBW rating categories and performance measures, to mention a few.

Based on its inhouse rating methodology, the EIF tranched the reference portfolio into a senior, mezzanine and junior tranches. The mezzanine tranche was assigned an internal rating of non-investment grade and priced at a gross price, which can’t be disclosed due to the private nature of the deal. In a synthetic securitisation transaction, the EIF directly fronts the guarantee vis-à-vis the counterpart. The guarantee is then counter-guaranteed by the EIB, which is the ultimate risk taker.

On the other hand, given that LBBW enters into a contractual undertaking to finance eligible new renewable energy projects, there’s a carrot and stick in the form of a retrocession payment from the EIB to LBBW for achieving allocations and reaching the new lending targets. Assuming LBBW generates twice the size of the mezzanine tranche, ie €350m of new financing, LBBW will receive a pre-defined retrocession amount from the EIB.

A majority of these payments must be used to provide an interest rate discount on the new lending. As a non-profit maximising supranational, the key for the EIB is the realisation of the new renewable energy projects. It should be recalled that the maturity of the new project finance loans is substantially longer than the maturity of the reference portfolio of loans to small and medium-sized companies and other corporates. In other words, the new project finance loans will still remain on LBBW’s balance sheet way longer than the securitisation transaction is outstanding.

A brief overview is provided in Figure 1.

Key risks and mitigants

Following the de-linked nature of the transaction, there are at least two separate areas of key risks and mitigants. To start with, guaranteeing a non-investment grade rated mezzanine tranche is by itself risky. A classical credit enhancement for the mezzanine tranche guarantee is an appropriate junior tranche or first loss piece below the mezzanine tranche. Further, in its structuring, the EIF uses a synthetic excess spread ledger that is placed below the junior tranche.

Regarding the new business generation, closing project finance transactions is an inherently complex and lengthy process. Given that only small and mid-sized project finance transactions are eligible under the EIB's intermediated approach, there needs to be several new project finance transactions originated and reported to the EIB. In addition, considering increasing interest rates in combination with falling economic activity in Germany, there are numerous challenges.

The mitigants to these risks consist of several different parts; to start with, the EIB involves a number of different specialised internal teams when performing its detailed due diligence. For example, one team of specialists come from the project directorate and are experts in eligibility, technology and legislation relating to a specific sector, in this case renewable energy. Approval is therefore only granted for transactions with counterparts with proven track-records, sufficient internal and external processes and procedures, and an appropriate pipeline. As part of LBBW’s commitment to generate new lending, a reporting template is agreed, and milestones are defined with minimum volumes. As part of the carrot and stick approach, a financial incentive in the form of conditional retrocession payments is embedded in the documentation structure.

While a key mitigant for the above-mentioned risks is clear and detailed contractual documentation, what’s probably even more important is a mutually trustful business relationship, ideally backed up by a strong track-record and know-how.

Key takeaways

This innovative transaction consists of both a synthetic securitisation transaction in combination with an undertaking to finance new renewable energy projects. By leveraging on the expertise of the EIB, the EIF and LBBW, the transaction makes a contribution to the green transition. The transaction is an example of “use of proceeds” securitisation whereby an existing loan book is used to support new green lending that is fully aligned with the EU taxonomy, ie a green securitisation.

EIB vice-president Ambroise Fayolle, who is responsible for operations in Germany, said: “Transactions like this one with LBBW support the decarbonisation of the energy sector and help the green transition to become a reality. I am glad that we can rely on LBBW as a trusted partner to provide the financial means needed by businesses in Germany in these challenging times.”

Dr Christian Ricken, a member of the executive management board of LBBW, said: “LBBW is extremely pleased that we can take our already very good partnership with the EIB to a new level with this transaction. At the same time, LBBW is underlining its commitment to proactively driving forward the green transformation of the economy.”

While EIB did not have an external legal counsel, LBBW was advised by Linklaters (Frankfurt) and EIF by Allen & Overy (London). The STS-certification of the synthetic securitisation transaction was done by STS Verification International and Deloitte is acting as verification agent.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com